The Internal Audit Process: A Brief Description

An internal audit usually follows this diagrammed pathway.

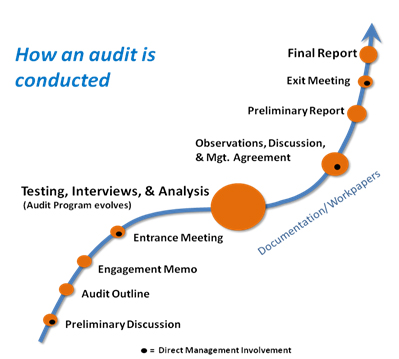

- Preliminary Discussion: About six weeks before an audit begins, the audit team talks with the leader of the area to be reviewed to confirm the schedule and begin to outline the work to be done.

- Audit Outline: The outline is a tool for planning an engagement. It includes the scope and objectives of the audit and begins to describe the kinds of interviews, analysis, document reviews and other procedures needed. The audit team prepares the outline about four weeks before the audit.

- Engagement Memo: About two weeks before the audit, the audit team sends the client a memo describing the engagement and confirming timing, location and anticipated needs.

- Entrance Meeting: At the beginning of the engagement, the audit team will meet with the primary leadership of the area to discuss scope, answer questions and begin the work.

- Testing, Interviews and Analysis: The auditors conduct interviews, analyze data, compare viewpoints and generally examine the subject area from top to bottom. As they do so, they compare the actual practices to standards or procedures in place. They also incorporate best/good practices to help evaluate whether processes are running optimally. If exceptions are identified, (the process is supposed to work one way but works another) these observations are collected and discussed with leadership of the area.

- Observations, Discussion, and Management Agreement: The auditor documents any observations and discusses the results with management. Sometimes management will clarify the observation; other times the auditor offers a recommendation for solving the issue. However, the best solutions often come from the leadership and their staff. Regardless of where the solution comes from, the auditor will ask the leadership to commit to a course of action and a date of completion. Auditors an only advise and report on the final decisions. They cannot make or change company policy.

- Preliminary Report: The auditor prepares a report. The report contains the purpose, scope, and results of the engagement. This report will be provided to the leadership for review and comment.

- Exit Meeting: Each audit ends with an exit meeting. Comments and corrections to the preliminary report are typically discussed and concluded at the exit meeting.

- Final Report: All final reports are copied to the leadership of the area, as well as to the manager, direct reports and board.

- Follow-up: Internal Audit tracks all issues identified during the engagement. It isn’t Internal Audit’s role to push for completion, but the department does have an obligation to track and report whether issues are getting resolved on time.